Q:How early should I begin shopping for a home if I hope to buy one this year?

There’s no hard-and-fast rule on how early to start looking for a home. But I suggest that first-time homebuyers give themselves at least six months.

Even with the rising number of more affordable homes going up for sale, it’s challenging to find a home you want in a location where you would like to live—and then beat out all of the competition for it.

Many buyers traditionally start home shopping around now as the spring housing market kicks off. Some will be lucky and have their first offer accepted, while others may be looking for years. How early you begin your search depends on your deadline to move, the number of buyers vying for homes in your area, and your price range.

It took the typical buyer 10 weeks to find a home, according to the most recent data from the National Association of Realtors®.

It might take you longer as there’s a lot of competition for move-in ready, affordable homes in a great school district. However, if you’re open to purchasing a fixer-upper, a home in a less popular location, or even a luxury home, your search might be considerably shorter. It’s really market-specific.

When my spouse and I purchased our first house, a starter home in the New York City suburbs, it took about nine months before we closed. This was in late 2021, though, during the COVID-19-juiced market. And we were holding out for that reasonably priced starter home with curb appeal.

If you’re thinking about starting your home search soon, there are a few things you should consider doing first.

1. Figure out what you can afford

The first thing first-time buyers should do is figure out how much home they can afford. There’s no point in falling in love with a home you can’t comfortably pay for. You also don’t want to get in over your head financially. (Repeat after me: I will not allow myself to be house poor.)

That’s why it’s helpful to run your numbers to help you to establish a budget. Don’t forget to factor in property taxes, home insurance, and private mortgage insurance (if you don’t put 20% down) costs as well.

Note: Property taxes can vary greatly from home to home and town to town. They can also rise steeply in some municipalities after you have work done on the property.

You can find out here how much home you can afford.

This might also be an opportune time to clean up your credit and pay down debt. Lenders typically grant larger loans to those with higher credit scores and less debt. Borrowers with pristine credit can also often score lower mortgage rates and fees on loans.

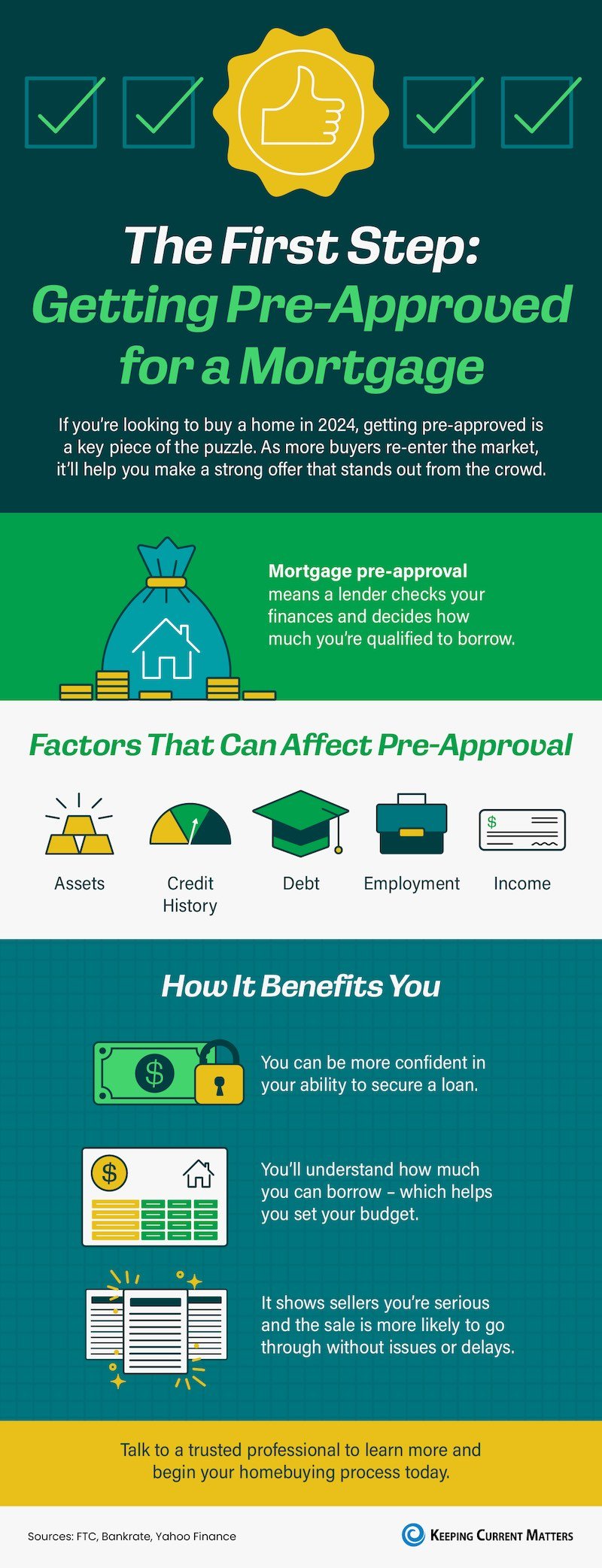

2. Get pre-approved for a mortgage

In the competitive spring market, you may need to act quickly if you see a great home. That’s why you should get a mortgage pre-approval letter early in your homebuying journey.

Most sellers aren’t going to want to take a chance on buyers who can’t prove they will be able to secure financing, especially if other offers come in. A pre-approval letter tells sellers that you’re serious—and are likely to be able to get a loan up to a specified amount.

3. Familiarize yourself with the local market

The more you know about the local market, the less time you’ll waste when you start putting in offers.

It helps to know how often homes in your price range are going up for sale and if they are located in neighborhoods where you would like to live. You’ll also want to know how quickly homes are selling in these areas, so you know if you need to make an offer on the spot or have some time to think it over.

Perhaps most importantly for first-time buyers, you should find out how much similar homes sold for at closing. Focus your research on homes in your price range in the places where you would like to live. If you want only a move-in ready home in a certain school district, look at those comps and not for fixer-uppers.

You’ll want to find out if these homes are selling for above the list price, and if so, by how much. Or maybe they’re not going for the asking price. This will help you to figure out the offers you should be making.

Try to be thorough in your research. What are the property taxes in this area? Is this area within a reasonable commute to your job? If you have children, are there other families in the neighborhood? Is the community close to parks and restaurants? You want to make sure this is a place where you’ll be happy.

4. Know your priorities

Finally, figure out what you have to have in a home—and what you can live without.

Unless you’re a multimillionaire, most first-time buyers will likely have to make some hard compromises. Knowing what you can live without or choosing a not-quite-ideal location could open up more potential homes. And if you’re looking in less competitive markets, you might be able to purchase a home faster.

For the original article by Clare Trapasso visit Realtor.com